Open Twitter on any given day and you'll see them. Screenshots of Polymarket accounts up 400%. Kalshi portfolios that turned $2,000 into $18,000 in three months. Threads from guys who "called" the election, the Fed decision, the Super Bowl, all within a few weeks. The replies are full of people asking for picks. Some of these accounts are selling Discord access for $99 a month.

Most of them are not good at this. They just got lucky. And the math proves it.

This isn't an insult. It's not saying they cheated or lied about their returns. The screenshots are real. The profits are real. What's fake is the idea that a few weeks or even a few months of winning tells you anything about whether someone actually has skill. Because when thousands of people are betting at the same time, some of them are going to look like geniuses by pure accident. That's not a bug in the system, it's a guarantee.

Let me walk you through why, with actual numbers, and then show you what real edge looks like so you stop sending money to random strangers on the internet.

What Variance Actually Means

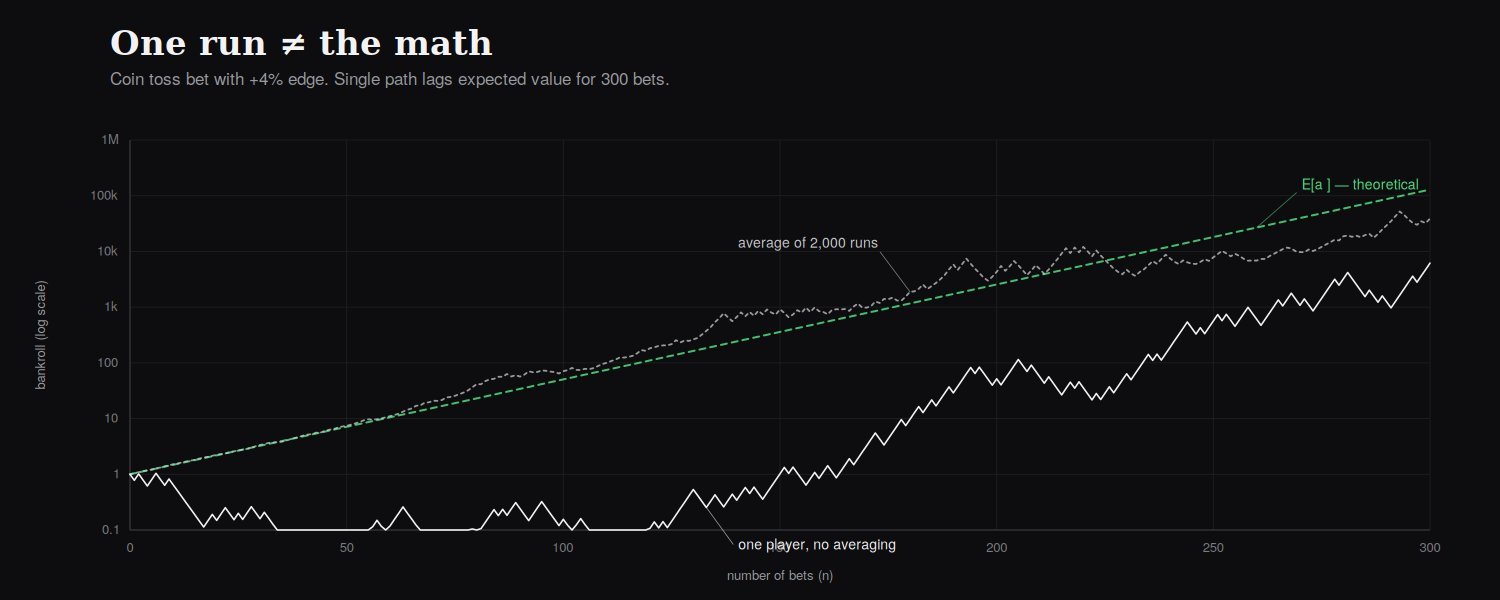

Variance is a fancy word for randomness. It's the gap between what "should" happen on average and what actually happens in any single stretch.

Flip a fair coin 10 times. On average you expect 5 heads and 5 tails. But if you actually try this, you'll sometimes get 7 heads and 3 tails. Sometimes 8 and 2. Once in a while, 9 and 1. The coin is not broken. You just didn't flip it enough times for the average to show up. Small samples lie. That's the whole concept.

Now picture 100 people each flipping a coin 10 times. Statistically, about 5 of them will get 8 or more heads. Another 5 or so will get 8 or more tails. If you only looked at the winners and ignored everyone else, you'd think you discovered 5 people with magical coin-flipping abilities. But you didn't. You just filtered for the lucky ones and pretended the unlucky ones don't exist.

This is called survivorship bias, and it's what's happening every time a prediction market trader goes viral. You see the winners. You don't see the 10,000 other accounts that blew up trying to do the same thing.

The Math on Polymarket and Kalshi

Let's put real numbers on this. Polymarket does hundreds of millions in monthly volume and has hundreds of thousands of active wallets. Kalshi has over a million users and keeps growing. Even if we assume most of them only bet a handful of times, you've still got a massive pool of bettors.

Say 50,000 people actively trade these platforms and each of them places 25 bets over a few months. Let's assume they're all completely clueless. They pick randomly and have a true win rate of exactly 50%.

Here's what happens. Out of those 50,000 random bettors, statistics say: roughly 2,000 of them will end up with 16 or more wins out of 25. That's a 64% win rate. Looks amazing. About 500 will end up with 18 or more wins. That's 72%. Screenshot-worthy. Around 75 will hit 20 or more wins. That's an 80% win rate over 25 bets, all with zero skill. And about 10 people will hit 22 wins or more. Those are the guys selling courses.

Every single one of these people is completely clueless in this simulation. But to their followers, to themselves, to anyone looking at their receipts, they look like savants. And this is with flat-odds 50/50 bets. On real markets with varying probabilities and parlays and creative bet selection, the distribution gets wider and weirder. More extreme winners, more extreme losers, and way more room for someone to look like Nostradamus for a while.

The point is not that nobody on these platforms is good. Some definitely are. The point is that just seeing someone up big tells you almost nothing, because you would expect a bunch of people to be up big even in a world where skill didn't exist at all.

A Concrete Example

In 2024, thousands of people bet on Polymarket's presidential election markets. Let's say someone went in on Trump at 52 cents and sold at 65, making solid returns. Then they hit on a few Senate races. Then they correctly called a Fed rate pause on Kalshi. Now they're up 180% and posting thread after thread about their process.

Is this person actually good? Maybe. But think about how many other people had identical trades. Tens of thousands of people bought Trump on Polymarket. Thousands bet on the Fed. The universe of people who could plausibly have made that same run of calls is huge. Some percentage of them are going to compound into spectacular returns just from stacking correct 50-60% probability bets. That's what probability does.

To really know if that person has an edge, you need way more data than one election cycle.

How Many Bets Do You Actually Need?

This is where it gets real, because the numbers are uncomfortable.

To tell the difference between a bettor who wins 50% of the time and one who wins 55% of the time, with any statistical confidence, you need roughly 400 to 500 resolved bets. And a 5% edge is already massive. Most professional sports bettors operate on 2-3% edges.

To identify someone with a 53% true win rate versus a 50% break-even bettor, you need closer to 1,000 resolved bets to be statistically confident you're not just looking at noise.

For a 52% win rate, which is still a profitable edge at reasonable odds, you basically need around 2,000 to 3,000 bets before variance settles enough for the true skill to show up clearly.

Let that sink in. Someone who has placed 40 bets and won 28 of them looks incredible, a 70% hit rate. But statistically, you cannot distinguish them from a 50% bettor who got lucky. A 70% hit rate over 40 bets has a p-value of around 0.008, which sounds significant, but think about how many bettors are out there. With 50,000 random bettors each placing 40 bets, you'd expect about 400 of them to hit 70% or better by chance. Four hundred "geniuses," all lucky.

What about 100 bets? Someone who goes 60-40 over 100 bets still isn't provably skilled. A random 50% bettor has about a 3% chance of doing that well. Out of thousands of bettors, plenty will hit that mark.

You really need several hundred bets minimum before you can start separating skill from luck. And most Twitter traders have not placed several hundred bets. They've placed 30. Or they've placed 200 but only post the winning ones.

So How Do You Actually Spot Edge?

Here's where profit charts become almost useless and other signals matter way more. If you're trying to figure out who actually knows what they're doing, here's what to look for.

Closing Line Value. This is the single most important metric and almost nobody on Twitter talks about it. Closing Line Value, or CLV, means the price you got a bet at compared to what that bet was trading at right before it resolved.

Example. You buy YES on a Kalshi market at 38 cents. Over the next two weeks, new information comes out, other traders pile in, and by the time the market closes, YES is trading at 67 cents. You got in at 38, the final market consensus was 67. You bought something for way less than the market eventually agreed it was worth. That's positive CLV.

Whether that specific bet won or lost is almost irrelevant. What matters is that you systematically bought things the market later priced higher, or sold things the market later priced lower. If you beat the closing line on 300 bets, you're almost certainly skilled, even if your profit is mediocre in that sample due to variance. If you consistently got worse prices than the closing line, you're losing money in the long run even if you happen to be up right now.

Professional sports bettors live and die by CLV. Lucky people do not consistently beat the closing line. They can't. If you're buying at random prices, you'll average out to the closing line, not beat it. Beating it means you saw something others didn't, repeatedly.

If a Twitter trader can't show you their CLV, they don't know if they're actually good. They just know they're up.

They can explain the trade in terms of mispricing. Ask a skilled trader why they made a bet and they'll talk about the market. "Polymarket had it at 18 cents but I had the real probability closer to 30. Even if I'm wrong half the time about my 30 number, I'm still paying way less than I should." Or "Kalshi was pricing this CPI print at 70% to come in below consensus, but I looked at the last six months of revisions and I think it's closer to 55%."

Notice what they're doing. They're not predicting the future. They're comparing their probability estimate to the market's probability, and betting when there's a gap. They might lose the bet. They often do. But every bet has positive expected value because they're paying less than they think something is worth.

A lucky trader tells you "I just had a feeling Trump would win" or "I knew the Chiefs couldn't lose that game." No framework, no probability estimate, no concept of what price would make a bet bad. They talk about outcomes. Sharps talk about prices.

If someone can't explain what price would have made them pass on the bet, they don't have a process. They have vibes. Vibes can print for a while. They do not print forever.

Their edge shows up in different kinds of markets. Real skill tends to transfer. Someone who's good at finding value understands how to decompose probabilities, how to avoid common biases, how to spot when a market is reacting to narrative instead of fundamentals. Those skills work across election markets, sports, economic data, celebrity events, whatever.

Be suspicious of someone who only performs in one narrow niche. Someone who destroys Kalshi's CPI markets every month but loses everywhere else probably has one useful model for one specific market, which is fine, but it's also a small edge that might not survive once others notice it. Someone who crushed Polymarket's 2024 election and then went quiet for 12 months probably caught one good wave.

The real ones tend to have a steady, boring track record across many different kinds of markets over a long period. Not explosive. Steady.

Their bet sizing is boring. Sharp traders size their bets based on two things: how big their edge is, and how big their bankroll is. There's a formula called the Kelly Criterion that spits out the optimal size. For most real-world edges of a few percent, Kelly tells you to bet 1-3% of your bankroll per bet. Sometimes less.

So a skilled trader with a $20,000 bankroll is placing $200 to $600 bets on spots they like. Occasionally bigger if the edge is massive. They do this hundreds of times because small edges compound through volume, not through hero bets.

Now look at the Twitter guys. Every single post is "MAX CONVICTION, THIS IS A LOCK, I'M ALL IN." That's not trading. That's gambling. Even if they have genuine edge on individual picks, the variance of betting 20% of your stack on every bet will eventually blow them up. The math is ruthless on this. You can have a 60% edge and still go broke if you bet too big, because one bad streak wipes you out.

If someone posts sizes that move with edge size, that's a good sign. If every bet is the same "huge" size regardless of the opportunity, they don't understand what they're doing, no matter how well it's going right now.

They show their losses too. Everyone has losing streaks. A 55% bettor loses 5 in a row about 2% of the time, which means it happens regularly over a career. A 53% bettor loses 6 in a row fairly often. If you're betting a few times a week, you'll hit ugly stretches every few months.

So any trader who's been at it seriously for more than a year has losing weeks, losing months, and embarrassing calls they'd rather forget. If someone's feed is 100% green screenshots, they're either very new, very dishonest, or very selective about what they post. Often all three.

The traders actually worth paying attention to post their losses, explain what went wrong, and update their process. They don't delete bad trades or mute replies when they're cold. They treat losing as information.

Their returns are not insane. If someone is claiming 500% annual returns on prediction markets, something is off. Even elite sports bettors with years of experience and private information target 10-30% ROI on turnover. On prediction markets, where liquidity is thinner and spreads are sometimes wider but opportunities are harder to scale, sustainable returns are in a similar range, maybe a bit higher for people willing to deal with the headache.

Anyone claiming they turn $10k into $100k reliably every year is either running one lucky streak they're about to lose, or they're not telling you the full story. Including the part where they were down 80% last year.

Quiet, boring, consistent returns over years are the signal. Screaming, explosive, "I can't believe this keeps working" returns over months are the noise.

What This Means for You

If you're trading Polymarket or Kalshi yourself, the honest answer is that you won't know if you're actually good for a long time. Place a few hundred bets, track your closing line value, write down why you made each bet before you made it, and see how your reasoning holds up. Most people don't do this because it's tedious and ego-bruising. Almost everyone who does it discovers they had less edge than they thought.

If you're thinking about following or paying someone for picks, stop looking at their P&L screenshots. They're almost useless. Ask how many bets they've resolved, not won. Ask if they track CLV. Ask them to walk through a losing trade and explain what they got wrong. Ask how they size. If they can't answer any of that, they're a gambler with good luck so far, not a trader with an edge.

And if you're one of those lucky ones right now, riding a positive variance streak and feeling like a genius, enjoy it, but be careful. The same math that let you win this fast will take it back if you mistake luck for skill and start betting bigger to chase it. The universe doesn't know it's supposed to keep rewarding you. It's just a coin flipping, and eventually the flips even out.

Being up is easy. Thousands of people are up right now for no reason other than chance. Being actually good at this is rare, takes years to prove, and usually looks a lot less sexy than the screenshots suggest.

That's the boring truth nobody posting their Polymarket PnL wants to tell you.